![]()

Jun 14, 2025 Step by Step Guide to Prepare for 8011 Exam BrainDumps

PRMIA Certification 8011 Real Exam Questions and Answers FREE Updated on 2025

NEW QUESTION # 119

What ensures that firms are not able to selectively default on some obligations without being considered in default on the others?

- A. Exchange listing requirements

- B. The bankruptcy code

- C. Chapter 11 regulations

- D. Cross-default clauses in debt covenants

Answer: D

Explanation:

It is the cross-default clauses in debt agreements that generally provide that a default on one obligation is considered a credit event applying to all debts of the obligor, and therefore we are able to deal with credit risk at the borrower level, and not at the level of the individual security. It also helps avoid situations where borrowers can selectively default on some obligations while continuing to service others. Therefore Choice 'a' is the correct answer. The other choices are incorrect.

NEW QUESTION # 120

Which of the following statements are true:

I. Common scenarios for stress tests include the 1997 Asian crisis, the Russian default in 1998 and other well known economic stress situations.

II. Stress tests provide the assurance that an institution's worst case losses will be covered.

III. Performing stress tests is highly recommended but is not mandated under Basel II.

IV. Historical events can be modeled quite accurately as they have defined start and end dates.

- A. I, III and IV

- B. All of the above

- C. I and II

- D. I only

Answer: D

Explanation:

Stress tests can cover known events, but since the future is unknown, and new events may be entirely different from what has happened in the past, they provide no assurance that an institution's worst case losses would be covered. Hence II is false.

Stress testing is required to be performed as part of Basel II, and therefore III is false.

Historical events do not have sharply defined start and end dates. Often, even after a crises ends, its after effects may continue to affect the markets for a long time. In such cases, it may be difficult to define the start and end of the crises. In many cases, the crises may persist for months or even years, making it difficult for the risk manager to identify a time period that covers the essence of the crises, and yet is focused enough to constitute a plausible scenario. Therefore IV is false too. Only I is true, and the correct answer is Choice 'b'.

NEW QUESTION # 121

Which of the following is not a tool available to financial institutions for managing credit risk:

- A. Credit derivatives

- B. Collateral

- C. Cumulative accuracy plot

- D. Third party guarantees

Answer: C

Explanation:

Collateral, limits to avoid credit exposure concentrations, termination rights based upon credit ratings, third party guarantees and credit derivatives are all tools or instruments that financial institutions use to manage their credit risk. A cumulative accuracy plot measures the accuracy ofratings, and is not a tool for managing credit risk. Therefore Choice 'b' represents the correct answer.

NEW QUESTION # 122

Which of the following statements is true:

I. Confidence levels for economic capital calculations are driven by desired credit ratings II. Loss distributions for operational risk are affected more by the severity distribution than the frequency distribution III. The Advanced Measurement Approach (AMA) referred to in the Basel II standard is a type of a Loss Distribution Approach (LDA) IV. The loss distribution for operational risk under the LDA (Loss Distribution Approach) is estimated by separately estimating the frequency and severity distributions.

- A. I, III and IV

- B. I, II and IV

- C. III and IV

- D. I and II

Answer: B

Explanation:

Statement I is correct. Economic capital is the capital available to absorb unexpected losses, and credit ratings are also based upon a certain probability of default. Economic capital is oftencalculated at a level equal to the confidence required for the desired credit rating. For example, if the probability of default for a AA rating is

0.02%, then economic capital maintained at a 99.98% would allow for such a rating. Economic capital set at a

99.8% level can be thought of as the level of losses that would not be exceeded with a 99.8% probability.

Loss distributions are the product of the severity and frequency distributions, each of which are estimated separately. The total loss distribution is affected far more by the severity distribution than by the frequency distribution, therefore statement II is correct.

The Loss Distribution Approach (LDA) is one of the ways in which the requirements of the AMA can be satisfied, and not the other way round. Therefore statement III is incorrect.

Statement IV is correct as the total loss distribution is estimated using separate estimates of loss frequency and distributions.

NEW QUESTION # 123

The minimum 'multiplication factor' to be applied to VaR calculations for calculating the capital requirements for the trading book per Basel II is equal to:

- A. 0

- B. 1

- C. 2

- D. 3

Answer: D

Explanation:

The minimum multiplication factor specified under Basel II is 3. Therefore the correct answer is Choice 'a'.

The exact requirements are laid down below.

Each bank must meet, on a daily basis, a capital requirement expressed as the higher of (i) its previous day's value-at-risk number measured according to the parameters specified in this section and (ii) an average of the daily value-at-risk measures on each of the preceding sixty business days, multiplied by a multiplication factor.

The multiplication factor will be set by individual supervisory authorities on the basis of their assessment of the quality of the bank's risk management system, subject to an absolute minimum of 3. Banks will be required to add to this factor a "plus" directly related to the ex-post performance of the model, thereby introducing a built in positive incentive to maintain the predictive quality of the model. The plus will range from 0 to 1 based on the outcome of so-called "backtesting."

NEW QUESTION # 124

Which of the following statements are true:

I. The sum of unexpected losses for individual loans in a portfolio is equal to the total unexpected loss for the portfolio.

II. The sum of unexpected losses for individual loans in a portfolio is less than the total unexpected loss for the portfolio.

III. The sum of unexpected losses for individual loans in a portfolio is greater than the total unexpected loss for the portfolio.

IV. The unexpected loss for the portfolio is driven by the unexpected losses of the individual loans in the portfolio and the default correlation between these loans.

- A. II and IV

- B. I and II

- C. I, II and III

- D. III and IV

Answer: D

Explanation:

Unexpected losses (UEL) for individual loans in a portfolio will always sum to greater than the total unexpected loss for the portfolio (unless all the loans are correlated in such a way that they default together).

This is akin to the 'diversification effect' in market risk, in other words, not all the obligors would default together. So the UEL for the portfolio will always be less than the sum of the UELs for individual loans.

Therefore statement III is true.This 'diversification effect' will be affected by the default correlations between the obligors, in cases where the probability of various obligors defaulting together is low, the UEL for the portfolio would be much less than the UEL for the individual loans. Hence statement IV is true.I and II are false for the reasons explained above.

NEW QUESTION # 125

Which of the following describes rating transition matrices published by credit rating firms:

- A. Probabilities of ratings transition from one rating to another for a given set of issuers

- B. Expected ex-ante frequencies of migration from one credit rating to another over a one year period

- C. Realized frequencies of migration from one credit rating to another over a one year period

- D. Probabilities of default for each credit rating class

Answer: C

Explanation:

Transition matrices are used for building distributions of the value of credit portfolios, and are the realized frequencies of migration from one credit rating to another over a period, generally one year. Therefore Choice

'd' is the correct answer.

Since they represent an actually observed set of values, they are not probabilities nor are they forward looking ex-ante estimates, though they are often used as proxies for probabilities. Choice 'a' and Choice 'c' are not correct. They include more than information on just defaults, therefore Choice 'b' is not correct.

NEW QUESTION # 126

The probability of default of a security during the first year after issuance is 3%, that during the second and third years is 4%, and during the fourth year is 5%. What is the probability that it would not have defaulted at the end of four years from now?

- A. 84.93%

- B. 88.53%

- C. 88.00%

- D. 12.00%

Answer: A

Explanation:

The probability that the security would not default in the next 4 years is equal to the probability of survival at the end of the four years. In other words, =(1 - 3%)*(1 - 4%)*(1 - 4%)*(1 - 5%) = 84.93%. Choice 'd' is the correct answer.

NEW QUESTION # 127

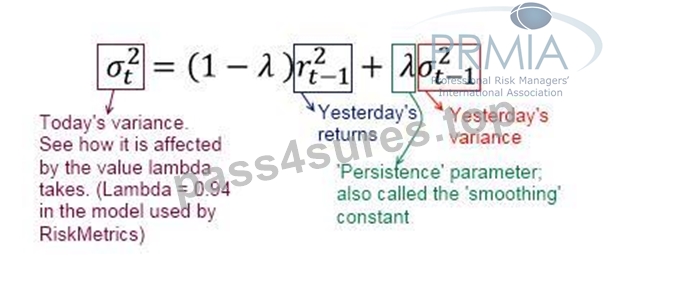

A stock's volatility under EWMA is estimated at 3.5% on a day its price is $10. The next day, the price moves to $11. What is the EWMA estimate of the volatility the next day? Assume the persistence parameter # = 0.93.

- A. 0.0018

- B. 0.0429

- C. 0.0421

- D. 0.0224

Answer: C

Explanation:

The correct answer is choice 'a'

Recall the formula for calculating variance under EWMA. See below. Therefore the correct answer is =SQRT ((1 - 0.93)*(LN(11/10))^2 + 0.93*((3.5%^2))) = 4.21%. Other answers are incorrect. Note that continuous returns are to be used, ie ln(11/10) and not discrete returns (=1/10) - though generally the difference between the two is small over short time periods. (If in the exam the answer doesn't exactly match, try using discrete returns.) A diagram of a mathematical equation Description automatically generated

NEW QUESTION # 128

A zero coupon corporate bond maturing in an year has a probability of default of 5% and yields12%. The recovery rate is zero. What is the risk free rate?

- A. 6.40%

- B. 5.26%

- C. 7.00%

- D. 5.00%

Answer: A

Explanation:

The probability of default would make the expected value of the future cash flows from both the corporate bond and the risk free bond identical. If p be the probability of default, the cash flows from the risky corporate bond would be

= (cash flows in the event of default x probability of default) + (cash flows without default x (1 - probability of default))

=> 5%*0 + (1 - 5%)*(1 + 12%) = (1 + Rf).

therefore Rf = 6.4%

(In reality investors would demand a 'credit risk premium' over and above the expected default loss rate. They are unlikely to be happy with just being compensated with exactly the expected default loss rate plus the risk- fre rate because the expected default loss rate itself is uncertain. They would demand some premium over and above what the default rate alone might mathematically imply above the risk free rate. In this question, this credit risk premium is ignored.)

NEW QUESTION # 129

For identical mean and variance, which of the following distribution assumptions will provide a higher estimate of VaR at a high level of confidence?

- A. A distribution with kurtosis = 2

- B. A distribution with kurtosis = 3

- C. A distribution with kurtosis = 8

- D. A distribution with kurtosis = 0

Answer: C

Explanation:

A fat tailed distribution has more weight in the tails, and therefore at a high level of confidence the VaR estimate will be higher for a distribution with heavier tails. At relatively lower levels of confidence however, the situation is reversed as the heavier tailed distribution will have a VaR estimate lower than a thinner tailed distribution.

A higher level of kurtosis implies a 'peaked' distribution with fatter tails. Among the given choices, a distribution with kurtosis equal to 8 will have the heaviest tails, and therefore a higher VaRestimate. Choice 'a' is therefore the correct answer. Also refer to the tutorial about VaR and fat tails.

NEW QUESTION # 130

Which of the following are attributes of a robust stress testing programme at a bank?

- A. Data of appropriate quality and granularity

- B. Written policies and procedures

- C. All of the above

- D. Robust systems infrastructure

Answer: C

Explanation:

A bank's stress testing programme in relation to firm wide stress tests should document the type, frequency and the purpose of the programme, as well as methodologies for defining scenarios and the remedial actions envisaged. Choice 'b' is therefore a necessary attribute of a robust stress testing programme.

The programme should be supported by a robust systems infrastructure that allows the execution of periodic as well as ad-hoc stress tests at the right level (business unit, as well as firm-wide) at the right level of detail or granularity. Choice 'c' also therefore is a valid choice.

A related element is data quality - without which no stress tests can be be credible.

Therefore all the choices listed are correct and Choice 'd' is the correct answer.

NEW QUESTION # 131

If an institution has $1000 in assets, and $800 in liabilities, what is the economic capital required to avoid insolvency at a 99% level of confidence? The VaR in respect of the assets at 99% confidence over a one year period is $100.

- A. 0

- B. 1

- C. 2

- D. 3

Answer: A

Explanation:

The economic capital required to avoid insolvency is just the asset VaR, ie $100. This means that if the worst case losses are realized, the institution would need to have a buffer equivalent to those losses which in this case will be $100, and this buffer is the economic capital.

The actual value of liabilities is not relevant as they are considered 'riskless' from the institution's point of view, ie they will be taken at full value. In this particular case, the institution has $200 in capital which is more than the economic capital required.

Therefore Choice 'c' is the correct answer.

NEW QUESTION # 132

Fill in the blank in the following sentence:

Principal component analysis (PCA) is a statistical tool to decompose a ____________ matrix into its principal components and is useful in risk management to reduce dimensions.

- A. Correlation

- B. Volatility

- C. Covariance

- D. Positive semi-definite

Answer: D

Explanation:

PCA is a statistical tool that decomposes a positive semi-definite matrix into its principal components. The first few principal components explain nearly all the variation and other components can then be ignored as they are too small in the larger picture. PCA in risk management is applied to a positive semi-definite correlation or covariance matrix to reveal the principal components that cause the variation. By allowing a focus on a few components, PCA reduces dimensionality.

While performing the math of PCA is unlikely to be asked in the PRMIA exam, you should remember that principal components have the additional property of being uncorrelated to each other which makes it useful as it is possible to vary one of the components without having to worry about the effect of that on the other components.

NEW QUESTION # 133

The degree distribution of the nodes of the financial network is:

- A. long tailed

- B. non-linear

- C. best approximated by a beta distribution

- D. normally distributed

Answer: A

Explanation:

The 'degree' of a node in a network measures the number of links to other nodes. For the financial network, each market participant can be thought of as a node. The 'degree distribution' can be thought of as the histogram of the number of links for each node.

The financial network has a degree distribution with rather long tails - and therefore Choice 'd' is the correct answer. The other choices are incorrect. Long tailed networks have the property that they are robust when affected by random disturbances, but susceptible to targeted attacks, for example on key hubs.

NEW QUESTION # 134

Changes in which of the following do not affect the expected default frequencies (EDF) under the KMV Moody's approach to credit risk?

- A. Changes in the debt level

- B. Changes in the firm's market capitalization

- C. Changes in the risk free rate

- D. Changes in asset volatility

Answer: C

Explanation:

EDFs are derived from the distance to default. The distance to default is the number of standard deviations that expected asset values are away from the default point, which itself is defined as short term debt plus half of the long term debt. Therefore debt levels affect the EDF. Similarly, assetvalues are estimated using equity prices. Therefore market capitalization affects EDF calculations. Asset volatilities are the standard deviation that form a place in the denominator in the distance to default calculations. Therefore asset volatility affects EDF too. The risk free rate is not directly factored in any of these calculations (except of course, one could argue that the level of interest rates may impact equity values or the discounted values of future cash flows, but that is a second order effect). Therefore Choice 'b' is the correct answer.

NEW QUESTION # 135

Which of the following statements are true:

I. Credit VaR often assumes a one year time horizon, as opposed to a shorter time horizon for market risk as credit activities generally span a longer time period.

II. Credit losses in the banking book should be assessed on the basis of mark-to-market mode as opposed to the default-only mode.

III. The confidence level used in the calculation of credit capital is high when the objective is to maintain a high credit rating for the institution.

IV. Credit capital calculations for securities with liquid markets and held for proprietary positions should be based on marking positions to market.

- A. II and III

- B. I and III

- C. I, III and IV

- D. I and II

Answer: C

Explanation:

Statement I is correct as credit VaR calculations often use a one year time horizon. This is primarily because the cycle in respect of credit related activities, such as loan loss reviews, accounting cycles for borrowers etc last a year.

Statement II is false. There are two ways in which loss assessments in respect of credit risk can be made:

default mode, where losses are considered only in respect of default, and no losses are recognized in respect of the deterioration of the creditworthiness of the borrower (which is often expressed through a credit rating transition matrix); and the mark-to-market mode, where losses due to both defaults and credit quality are considered. The default mode is used for the loan book where the institution has lent moneys and generally intends to hold the loan on its books till maturity. The mark to market mode is used for traded securities which are not held to maturity, or are held only for trading.

Statement III is correct. The confidence interval, or the quintile of losses used for maintaining credit ratings tends to be very high as the possibility of the institution's default needs to be remote.

Statement IV is correct too, for the reasons explained earlier.

NEW QUESTION # 136

For a back office function processing 15,000 transactions a day with an error rate of 10 basis points, what is the annual expected loss frequency (assume 250 days in a year)

- A. 0

- B. 1

- C. 2

- D. 0.06

Answer: B

Explanation:

An error rate of 10 basis points means the number of errors expected in a day will be 15 (recall that 100 basis points = 1%). Therefore the total number of errors expected in a year will be 15 x 250 = 3750. Choice 'a' is the correct answer.

NEW QUESTION # 137

When building a operational loss distribution by combining a loss frequency distribution and a loss severity distribution, it is assumed that:

I. The severity of losses is conditional upon the number of loss events II. The frequency of losses is independent from the severity of the losses III. Both the frequency and severity of loss events are dependent upon the state of internal controls in the bank

- A. II and III

- B. I and II

- C. I, II and III

- D. II

Answer: D

Explanation:

When a operational loss frequency distribution (which, for example, may be based upon a Poisson distribution) and a loss severity distribution (for example, based upon a lognormal distribution), it is assumed that the frequency of losses and the severity of the losses are completely independent and do not impact each other. Therefore statement II is correct, and the others are not valid assumptions underlying the operational loss distribution.

NEW QUESTION # 138

......

Ultimate Guide to Prepare 8011 Certification Exam for PRMIA Certification: https://www.pass4sures.top/PRMIA-Certification/8011-testking-braindumps.html

8011 Ultimate Study Guide: https://drive.google.com/open?id=1bNnxBnJe4lSbH1Zzu0M5HIizy9A8skps